LAB Pro

Project cost management is often reduced to budget monitoring, even though broader project dynamics shape cost outcomes. Understanding how planning, execution, and decision-making interact provides a more meaningful basis for evaluating project success. This article analyzes how project performance domains can serve as a practical framework for cost analysis and support a more comprehensive evaluation of project performance.

Authors: Saara Aksola & Taina Savonen

Project Performance Domains as a Framework for Cost Management

The PMBOK® Guide (2025) defines eight project performance domains that guide project execution. Rather than focusing on isolated processes, the domains form an integrated system that emphasizes value delivery.

A key observation is that cost management does not belong to a single domain. Instead, cost performance emerges from the interaction of multiple domains throughout the project lifecycle (Aksola 2026). Although cost is not explicitly defined within the domains, their activities continuously influence cost development.

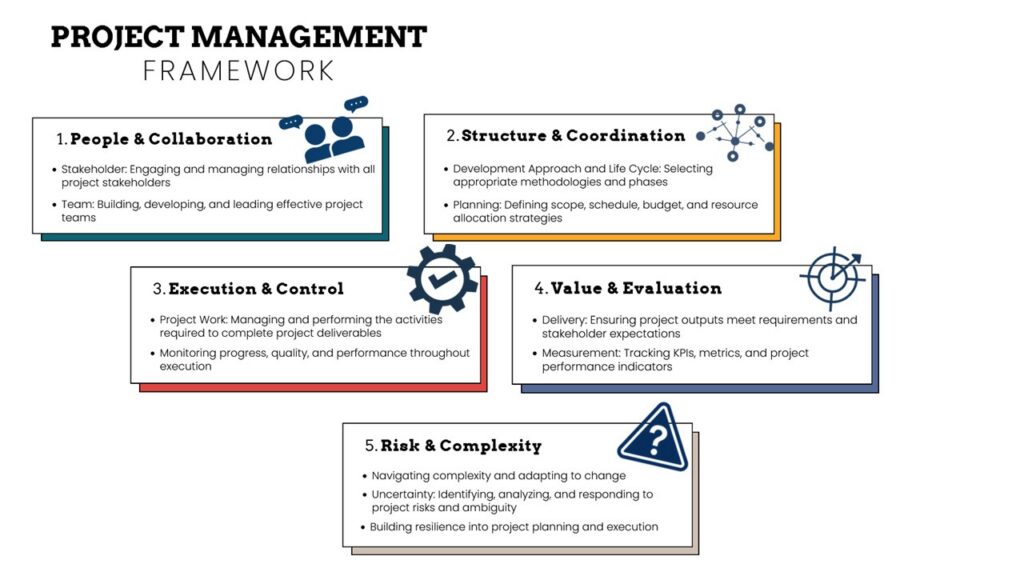

Together, the domains represent the key areas that must be addressed to ensure successful outcomes. They function as an interconnected system, where changes in one domain inevitably affect others (Figure 1). Figure 1 illustrates how the domains can be grouped based on their roles in project execution.

Figure 1. Project performance domains and their descriptions (mod. PMBOK® Guide 2025) mapped to project management framework.

The stakeholder domain focuses on identifying, analyzing, and actively engaging stakeholders throughout the project, while the team domain emphasizes building and supporting a collaborative and accountable project team through leadership and shared responsibility. Together, these domains form the broader perspective of People & Collaboration.

By integrating the development approach and life cycle domain with the planning domain, a broader perspective of Structure & Coordination emerges. The development approach and life cycle domain define how project work is structured over time, taking into account the project context, uncertainty, and value delivery needs. Complementing this, the planning domain aligns and coordinates project activities by integrating scope, schedule, cost, resources, risks, and communication into a coherent framework that supports decision-making (PMBOK® Guide 2025).

For Execution & Control, the project work domain focuses on managing and carrying out project activities, including resource coordination, communication, change control, and knowledge sharing. This also refers to monitoring project progress, quality of project outcomes, and team performance throughout the execution. (PMBOK® Guide 2025.)

The delivery and measurement domains together form the category of Value & Evaluation. The delivery domain ensures that project outputs meet defined requirements and fulfill stakeholder expectations, while emphasizing quality and value realization. The measurement domain supports this by tracking performance through relevant indicators and enabling transparent, evidence-based decision-making. Together, these domains ensure that project progress and value delivery can be continuously assessed (PMBOK® Guide 2025).

Finally, the uncertainty domain addresses risks, ambiguity, and complexity by promoting the proactive identification of uncertainties and systematic responses to both threats and opportunities throughout the project lifecycle (PMBOK® Guide 2025).

Evaluating and Improving Project Performance

From a cost management perspective, the planning, measurement, and project work domains form the foundation for control (Aksola 2026). Planning defines cost baselines that act as reference points, while measurement enables continuous tracking through key performance indicators. Without these baselines, cost performance cannot be meaningfully assessed. (PMBOK® Guide 2025.)

During execution, the project work domain plays a central role in determining actual cost outcomes. Change management and other control practices directly influence whether the project stays within budget. Tools such as Earned Value Management (EVM) support monitoring by combining cost, schedule, and scope information. For example, the Cost Performance Index (CPI) indicates whether spending aligns with achieved progress (Pelin 2020).

At the end of the project, performance domains can be assessed by comparing actual outcomes with initial objectives and analyzing deviations encountered during execution (Aksola 2026). Final cost analysis provides an overall view of project performance, including differences between planned and actual costs, execution efficiency, and the effectiveness of decision-making. Linking these insights to domain performance helps clarify their impact on profitability.

This perspective shifts cost management from reactive budget tracking to proactive performance management. By using performance domains as an analytical framework, organizations can identify critical turning points where cost divergence begins. At the same time, it supports better pricing decisions, improves project execution practices, and strengthens continuous learning.

Conclusion

Project performance domains provide a structured and practical way to understand cost behavior. Instead of treating costs as isolated figures, they highlight how project activities influence financial outcomes.

Applying this approach supports better decision-making and contributes to improved project profitability (Aksola 2026). Ultimately, it invites organizations to rethink not only how costs are managed, but how project success is truly understood.

References

Aksola, S. 2026. Cost Analysis Method Development and Project Performance Evaluation for Improving Project Pricing. Master’s Thesis. LAB University of Applied Sciences, Business Innovation Culture and Creativity. Cited 24 May 2026. Available at https://urn.fi/URN:NBN:fi:amk-2026051712799

Pelin, R. 2020. Projektihallinnan käsikirja. 8th edition. Helsinki: Projektijohtaminen Oy Risto Pelin.

PMBOK Guide. 2025. A Guide to the Project Management Body of Knowledge (PMBOK® Guide) – Seventh Edition and The Standard for Project Management. Newton Square (PA): Project Management Institute (PMI).

Authors

Saara Aksola is a Master of Business Administration student at LAB University of Applied Sciences. The article is based on her thesis, which concludes her studies.

Taina Savonen is a Senior Lecturer in Business at LAB University of Applied Sciences and actively contributes to projects, offering practical insight into project performance and development.

Illustration: https://www.pexels.com/photo/people-creative-office-working-6773652/ (Pexels Licence)

Reference to this article

Aksola, S. & Savonen, T. 2026. Beyond Budget Tracking: Rethinking Project Cost Performance. LAB Pro. Cited and date of citation. Available at https://www.labopen.fi/lab-pro/beyond-budget-tracking-rethinking-project-cost-performance/